How Interest Rates Impact Covered Calls

How rising and falling interest rates change covered call premiums and practical adjustments to strike, expiration, and stock choice to protect income.

Covered calls vs cash-secured puts both let you earn income by selling options on stocks you already own. But did you know interest rates directly affect the premiums you can collect? Here’s the quick takeaway:

- Rising interest rates increase call option premiums, meaning higher income for sellers. This happens because higher rates raise the cost of buying stocks outright, making options more attractive.

- Falling interest rates reduce premiums, shrinking your income potential. Lower rates make holding cash or buying stocks cheaper, decreasing the appeal of options.

To adjust, tweak your strategy:

- In high-rate environments, focus on out-of-the-money (OTM) options and longer expiration dates for higher premiums. This strategy leverages how time decay impacts your position as it approaches maturity.

- In low-rate conditions, shift to shorter expirations, closer-to-the-money strikes, and high-volatility or dividend-paying stocks to maintain income.

Understanding the connection between interest rates and covered calls helps you maximize returns, whether rates are climbing or falling.

How Interest Rates Impact Covered Call Premiums and Strategy

How Rising Interest Rates Affect Covered Calls

When interest rates rise, selling covered calls becomes more appealing due to the higher premiums available. This creates opportunities for investors to increase their income from stocks they already own. Let’s break down why this happens and how to adjust strategies to take advantage.

Higher Interest Rates Increase Call Option Premiums

As interest rates climb, the cost of tying up capital in stocks increases. This makes call options more appealing to buyers, as they offer a capital-efficient alternative. The relationship between interest rates and option prices is quantified by rho, one of the option Greeks. Hamilton Reiner, Portfolio Manager and Head of U.S. Equity Derivatives at JP Morgan Asset Management, explains:

Higher rates make calls more expensive... That's good for those selling the options.

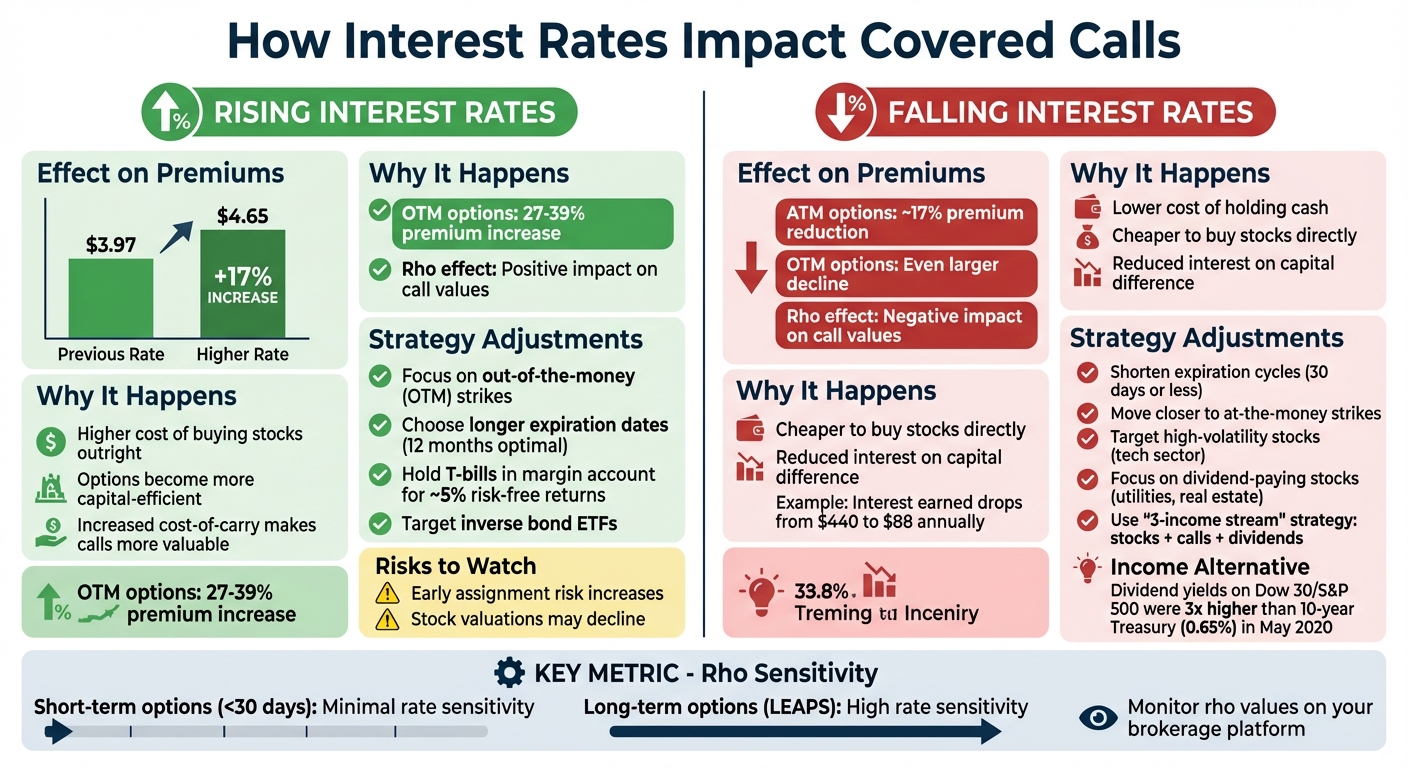

The data backs this up. In October 2023, Exceed Advisory analyzed a hypothetical $100 stock with 20% volatility and 90 days to expiration. By raising the risk-free interest rate from 0.053% (January 2022) to 5.49% (October 2023), the theoretical call price increased from $3.97 to $4.65 - a 17% jump in premium for covered call sellers. Out-of-the-money (OTM) options were even more sensitive, with premiums increasing by 27–39% as rates rose.

Benefits and Risks in a High-Rate Environment

Higher premiums provide a cushion against potential stock price declines. Additionally, investors can enhance returns by holding T-bills in a margin account to earn interest while simultaneously selling covered calls on their stock positions. For example, in late 2023, during a period of elevated rates and market volatility, a 77-day call option on the S&P 500 with a 3% OTM strike offered a premium of $5.06 - equivalent to 1.10% of the underlying value.

However, there are risks to consider. Rising rates can pressure stock valuations, as higher discount rates lower the present value of future cash flows and make fixed-income investments more attractive. There’s also a heightened risk of early assignment on in-the-money positions, as option holders may want to capitalize on the increased interest earned from an early sale.

Adjusting Strike Prices and Expiration Dates

To make the most of higher premiums, it’s worth tweaking your option parameters. Focus on out-of-the-money strikes rather than at-the-money options. OTM options are more sensitive to interest rate changes, capturing a larger percentage of the premium increase.

Opting for longer expiration dates can also amplify premiums. While 30–45 day options are popular for their time decay benefits, longer-dated options - especially those with 12 months to expiration - are more responsive to interest rate changes and generate higher premiums. On the other hand, options with less than 30 days to expiration show minimal sensitivity to rate changes. If you’re targeting gains in a high-rate environment, longer durations might be the better choice.

These adjustments can help maximize income from covered calls, making them a valuable strategy in a rising interest rate landscape.

sbb-itb-a9ac3c2

How Falling Interest Rates Affect Covered Calls

Falling interest rates can be a headache for covered call sellers. As rates drop, so do the premiums you can collect, making it harder to generate income. To navigate this challenge, it’s important to understand why premiums shrink and how to tweak your strategy to keep your returns steady. Lower premiums not only cut into your income but also push you to rethink your approach to options.

Lower Interest Rates Reduce Call Option Premiums

The relationship between interest rates and call premiums is tied to a concept called positive rho. Simply put, when interest rates fall, call premiums follow. Scott Fullman, The Strategist at IVolatility, explains:

As the cost-of-carry increases, so do the premiums for call option contracts. Conversely, the premiums for call options decline as interest rates fall.

Here’s why: buying a call option requires much less capital than buying the underlying stock outright. For example, purchasing 100 shares of a $100 stock costs $10,000, while a call option on the same stock might cost just $1,200. If interest rates drop from 5% to 1%, the interest earned on the $8,800 capital difference falls from $440 to just $88 annually. This makes the call option less appealing - and less valuable.

The extent of this impact depends on the type of option. A 1% change in interest rates typically alters an option’s price by its rho. For at-the-money options, a steep drop in the risk-free rate can reduce premiums by roughly 17%. Out-of-the-money options take an even bigger hit. For covered call sellers, this directly translates to lower income from premiums.

Strategies for Maintaining Returns When Premiums Drop

When premiums shrink due to falling rates, you can still maintain your income by adjusting your approach. Here are some strategies to help you adapt:

- Shorten expiration cycles. Options with shorter terms - like those expiring within 30 days - are less sensitive to interest rate changes compared to long-term options such as LEAPS. Using weekly or monthly expirations can help reduce the impact of falling rates.

- Adjust strike prices. Out-of-the-money options lose value faster when rates drop. By moving closer to the money - say, from a 10% OTM strike to an at-the-money strike - you can capture more premium, even if it slightly increases the chance of assignment.

- Target high-volatility stocks. Implied volatility has a much stronger influence on option premiums than interest rates. Focusing on stocks with higher volatility, such as those in the tech sector, can help offset the loss in premiums caused by lower rates.

- Focus on dividend-paying stocks. Dividend-paying sectors like utilities and real estate can provide an additional income stream. Alan Ellman, President of The Blue Collar Investor, suggests a "3-income stream" strategy for low-rate environments:

In a low-interest rate scenario... we can set up a low-risk, 3-income stream strategy using blue chip stocks, out-of-the-money call options and dividend capture for each position.

For example, during May 2020, when the 10-year Treasury yield was just 0.65%, dividend yields on Dow 30 and S&P 500 stocks were three times higher than the Treasury. Combining dividend capture with covered call writing can help you maintain your overall returns, even as option premiums shrink.

Adjusting Your Strategy for Interest Rate Changes

Interest rate movements can significantly impact option premiums, and knowing how to adapt your strategy is essential. The trick lies in identifying which sectors thrive under these conditions and using the right tools to uncover opportunities.

Portfolio Diversification and Sector Selection

Diversifying your portfolio is a smart way to manage risk, especially given how different sectors react to interest rate changes. For instance, when rates rise, inverse bond ETFs often perform well, making them ideal for covered call writing. These ETFs tend to gain value as bond prices drop.

Take December 2010 as an example. With rates expected to climb, the ProShares UltraShort Barclays 20+ Year ETF (TBT) became a popular choice for covered calls due to its liquidity and inverse relationship with bond prices. A specific trade involved selling January 36 calls at $37.04, resulting in a net debit of $35.34. This setup offered a theoretical annualized return of 31.5% if the ETF's price remained flat. Since TBT uses 2x leverage, opting for strike prices one or two levels deeper in-the-money can help manage the added volatility.

Another effective approach in high-rate environments is cash stacking. By holding T-bills in a margin account, you can earn around 5% in risk-free returns while simultaneously generating additional income by selling covered calls. Schaeffer's Investment Research explains:

The saved capital... can be put into a risk-free asset such as a T-bill to generate interest, allowing the trader to benefit from the potential upside of a stock and generate income with a bond.

Using Tools to Find Better Covered Call Opportunities

Beyond choosing the right sectors, leveraging analytical tools can refine your strategy. These tools help identify high-quality covered call candidates and assess how interest rate sensitivity impacts your positions.

Platforms like ThetaEdge provide AI-driven insights tailored to your holdings. This includes evaluating risk/reward metrics and assignment probabilities, making it easier to spot the covered call opportunities in fluctuating rate environments. For instance, ThetaEdge tracks rho - a measure of an option's sensitivity to interest rate changes - helping you optimize your trades, especially for long-dated options.

Additionally, many brokerage platforms, including Fidelity, TradeStation, and Tradier, allow you to add rho to your options chains. While rho has minimal impact on short-term options expiring within a month, it becomes crucial when trading LEAPS or other long-dated calls. These options are much more sensitive to rate changes, making rho an essential factor to monitor.

Conclusion

Key Takeaways for Investors

Understanding how interest rates influence covered calls can give you an advantage in managing your portfolio. As rates rise, call premiums increase due to the positive rho effect, which means higher income potential from your investments. Historical trends back this up, showing noticeable premium growth during periods of rising rates.

Adapting your strategy to match the current rate environment is essential. In high-rate scenarios, consider writing covered calls with farther out-of-the-money strikes, as these options tend to be more responsive to rate changes. You can also enhance your income by holding T-bills in your margin account while selling calls, allowing you to earn risk-free interest alongside option premiums. Conversely, when rates decline, it may be wise to diversify into sectors that perform better in low-rate environments and adjust your strike prices to maintain steady income.

Keep an eye on early assignment risks in high-rate conditions. Pay particular attention to rho values, especially for long-term options like LEAPS, as their pricing can be heavily influenced by rate sensitivity. Adjusting your approach with covered call risk management strategies and tools is key to navigating these shifts effectively.

Using ThetaEdge for Better Covered Call Analysis

Managing these variables - like tracking rho sensitivity, calculating the cost of carry, and identifying the best strikes - can be daunting without the right tools. This is where ThetaEdge comes in, offering AI-driven analysis tailored to your portfolio needs.

ThetaEdge provides real-time insights into how interest rates impact covered calls. It evaluates risk/reward metrics and tracks rho sensitivity, particularly for longer-dated options, helping you identify the most profitable strikes and expiration dates. With Thetix, the platform's AI assistant, you can get answers to portfolio-specific questions and receive daily action plans to maximize your income, no matter which direction interest rates are heading.

FAQs

How do Fed rate changes affect covered call pricing?

When the Federal Reserve adjusts interest rates, it directly influences covered call pricing through a metric known as Rho. Rho reflects how sensitive an option's price is to a 1% change in interest rates. Generally, when the Fed increases rates, call option premiums tend to rise, while put option premiums often decline. However, the precise impact varies depending on the specific option and the strategy in play.

When do interest rates matter more than volatility for call premiums?

Interest rates play a bigger role than volatility in determining call premiums when changes in rates - captured by rho - have a meaningful impact on an option's value. This effect becomes more pronounced over longer time periods or during periods of higher interest rates. On the other hand, volatility mainly affects the time value of an option, making it a stronger factor in short-term trading scenarios.

How can I reduce early assignment risk when rates are high?

In a high-rate environment, reducing early assignment risk involves a couple of strategic adjustments. First, choosing strike prices that are further out-of-the-money can create a larger cushion before your stock might be called away. This extra buffer can be especially helpful when rates are high. Additionally, focusing on shorter expiration periods can minimize your exposure to interest rate fluctuations, which could otherwise increase the likelihood of early assignments. Together, these strategies aim to strike a balance between generating income and managing the risk of positions ending prematurely.