Rolling Covered Calls: Risk and Reward Analysis

Rolling covered calls is a trade-off, not an escape: it changes income, upside cap, and assignment risk without fixing stock risk.

Rolling a covered call does not fix a bad stock trade. It only changes three things: income, upside cap, and assignment odds.

If I roll, I’m making a new trade. That means I need to ask:

- Do I still want to own the stock here?

- Am I getting enough new premium to justify more time in the trade?

- Am I paying too much just to avoid assignment?

- Will the new expiration run into earnings, dividends, taxes, or more slippage?

Here’s the short version:

- A roll out gives me more time and usually more premium, but keeps my upside capped.

- A roll up gives me more room on the upside, but often costs a net debit.

- A roll down brings in more premium after a drop, but lowers my sale price and can lock in a loss if assigned below cost basis.

- A roll up-and-out tries to do both: more upside room and more time. That can work, but it still ties up capital longer.

A covered call strategy always has the same payoff shape. I collect premium up front, lower my breakeven by that amount, cap gains above the strike, and still take almost all the stock downside.

If I bought shares at $50.00 and sold a $55.00 call for $1.50, my breakeven drops to $48.50, but my max gain is still capped once the stock gets above $55.00.

The main point is simple: rolling is a trade-off, not an escape hatch. Sometimes the best move is to roll. Sometimes it’s better to let the shares get called away. Sometimes it’s better to close the position and move on.

Quick Comparison

| Roll Type | What I Change | Main Goal | Main Risk |

|---|---|---|---|

| Roll Out | Later expiration, same strike | More premium, more time | Cap stays in place longer |

| Roll Up | Higher strike, same expiration | More upside room | Often costs cash |

| Roll Down | Lower strike, same expiration | More premium after a drop | Lower cap, higher chance of assignment |

| Roll Up-and-Out | Higher strike, later expiration | More upside room plus more time | More time in trade, mixed credit/debit |

A good roll should put me in a better next trade, not just delay a choice I don’t want to make.

sbb-itb-a9ac3c2

The Problem With Static Covered Calls

A covered call can work fine when the stock stays near the range you expected. The trouble starts when the stock moves hard in either direction. At that point, a static position gets tougher to manage as expiration gets closer.

When the stock rallies past the strike

This is the frustration most investors run into first. The stock pushes well above the strike price, the call goes deep in the money, and your upside is capped no matter how much higher the shares run.

Here’s a real example from May 2026. An investor holding Apple (AAPL) shares with a $190 cost basis sold a $200 strike call expiring May 31 for a $4.10 premium. By May 22, AAPL had climbed to $205, and the call was worth $5.30. If the shares were assigned at $200, the gain would have been capped at $14.10 per share. To keep the shares, the investor had to roll up-and-out to a June 28 $210 strike, which required a $0.10 net debit and pushed the effective sale price to $214.

That’s the whole problem in plain English: the stock keeps going up, but gains above the strike are no longer yours.

The same static setup creates a different headache when the stock drops.

When the stock falls and the premium is not enough

A covered call can cushion losses by the amount of premium you collect. It does not remove the downside in the stock itself.

One contract on a $400 stock controls 100 shares, or $40,000 worth of stock. That gap matters. The premium may look nice upfront, but a sharp drop in the shares can swamp that income fast. Rolling down after a decline may improve your breakeven a bit, but it does not undo the loss already sitting in the stock. And if the new strike ends up below your cost basis, assignment at that level can lock in a guaranteed loss.

So even when the call brings in income, the stock position still does most of the heavy lifting - for better or worse.

Assignment risk, ex-dividend dates, and expiration pressure

Even if the stock barely moves, timing risk can still force your hand before expiration.

As expiration gets closer, gamma risk rises. That means the option price reacts more sharply to small moves in the stock. A position that looked under control two weeks earlier can shift fast in the last few days.

Early assignment also becomes more likely when a call is in the money and has very little time value left. Ex-dividend dates add another layer of risk. If the dividend is larger than the call’s remaining time value, early assignment becomes more likely. That can blindside investors who are not watching the dividend calendar.

In the final days before expiration, bid-ask spreads often widen, and slippage can make a roll look much worse than it did on paper. That’s usually when the roll-or-accept-assignment choice stops being theoretical and becomes immediate.

That is where rolling starts to matter. You can use AI-powered portfolio analysis to model these scenarios before you commit to a trade.

What Rolling Changes and What It Does Not Fix

Rolling is a buy-to-close and sell-to-open adjustment that changes the strike, the expiration, or both. When the original call no longer matches the stock move, a roll pushes the exit decision forward. It does not solve the underlying trade by itself.

That’s the key idea. The question isn’t whether you can roll. It’s whether the new position gives you a better next trade.

Roll out, roll up, roll down, and roll up-and-out explained

Each roll type does a different job:

| Roll Type | Strike Change | Expiration Change | Primary Goal |

|---|---|---|---|

| Roll Out | Same | Later | Extend income; buy more time |

| Roll Up | Higher | Same | Capture more stock upside |

| Roll Down | Lower | Same | Collect more premium after a drop |

| Roll Up-and-Out | Higher | Later | Raise the cap while extending time |

A roll up often comes with a net debit. You pay to move the strike higher so you can keep more upside if the stock keeps climbing.

A roll down does the opposite. It brings in more premium after the stock falls, but it also cuts your maximum profit. If assignment happens below your cost basis, it can also lock in a realized loss.

A roll up-and-out tries to do two things at once: lift the cap and add more time. That can help, but there’s no free lunch here. Every roll swaps one set of trade-offs for another.

What rolling can change versus what stays the same

Rolling can change:

- Strike price

- Expiration date

- Net premium collected

- Assignment odds

What it does not change is just as important. It does not change the stock’s path. It does not remove downside on the shares. Your stock position still drives the P&L.

That’s where many traders get tripped up. The option terms move around, but the main engine of the trade is still the stock.

Costs, taxes, and slippage that can reduce the benefit

A roll only makes sense if the net result still beats the other choices. That means you have to account for the friction in the trade, not just the headline premium.

Commissions, per-contract fees, and bid-ask slippage hit both legs. And timing matters. Rolling in the last few days before expiration is generally inefficient because slippage alone can be more than the remaining time premium.

Taxes can also change the math. Each roll creates one closing event and one opening event for tax purposes. It may also affect qualified covered call status and holding-period treatment.

Risk and Reward Analysis of Common Roll Decisions

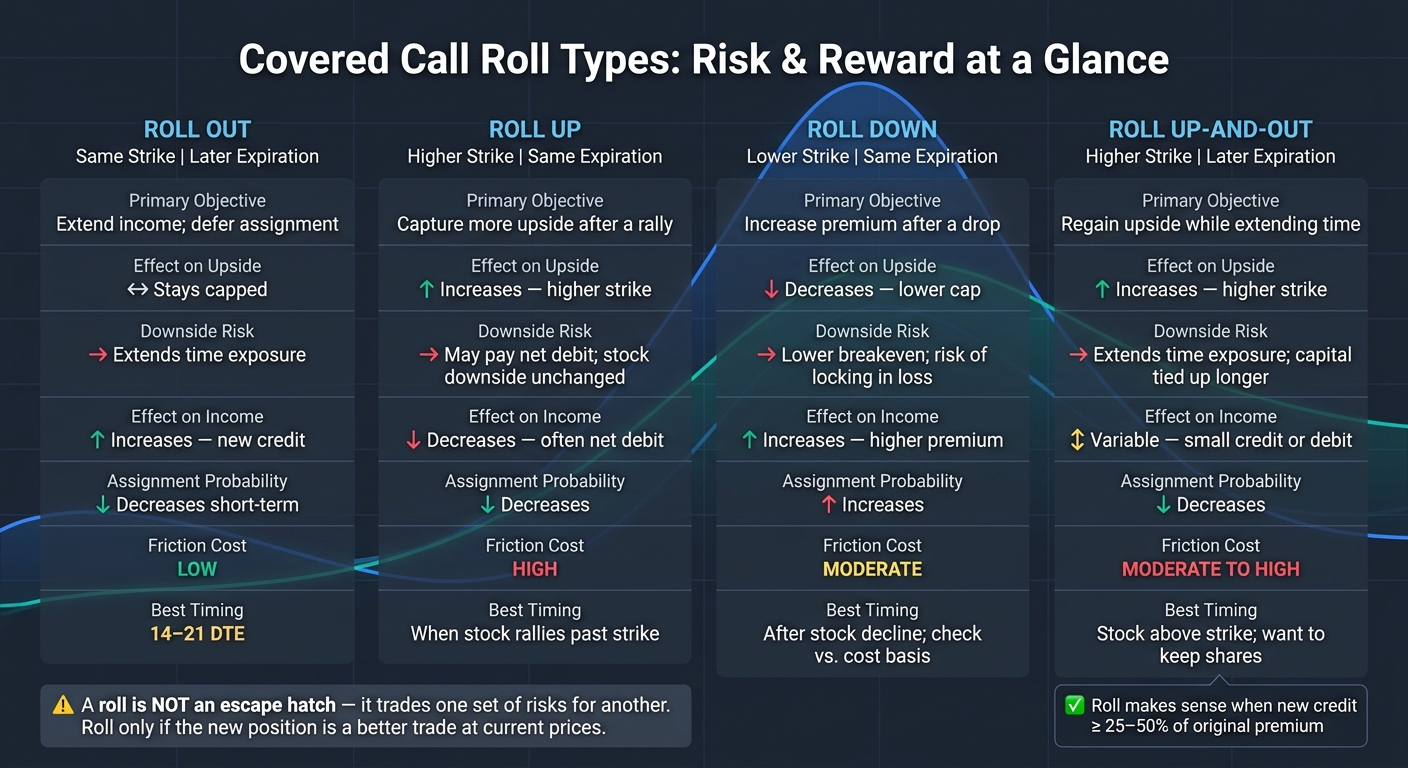

Covered Call Roll Types: Risk & Reward Comparison

Every roll shifts the trade-off. Some give you more time. Some give you more room on the upside. Others squeeze out more premium. The best move depends on what matters most right now: income, upside, or assignment risk.

Once the position changes, the next step is matching the roll to that new setup.

| Roll Out | Roll Up | Roll Down | Roll Up-and-Out | |

|---|---|---|---|---|

| Primary Objective | Extend income; defer assignment | Capture more upside after a rally | Increase premium after a drop | Regain upside while extending time |

| Effect on Upside | Stays capped at the same strike for longer | Increases (higher strike) | Decreases (lower strike) | Increases (higher strike) |

| Downside Risk | Extends time exposure | Slightly worse if you pay a debit; stock downside remains unchanged | Lower breakeven | Extends time exposure |

| Effect on Income | Increases (new credit) | Decreases (often a net debit) | Increases (higher premium) | Variable (small credit or debit) |

| Assignment Probability | Decreases short-term | Decreases | Increases | Decreases |

| Friction Cost | Low | High | Moderate | Moderate to High |

Rolling out: more time premium, longer upside cap

If you still want to hold the shares and you're fine with the current strike, rolling out is the plainest move. You keep the same cap, but you give the trade more time to play out. That can mean more premium, but it also means the position has more time to move against you.

Rolling at 14–21 DTE often leaves enough time value to produce a net credit. Waiting until only 1–2 DTE is usually bad timing because bid-ask spreads tend to widen and slippage gets worse.

Rolling up or up-and-out: regaining upside at a price

When the stock is already above the strike, rolling up only makes sense if the extra upside is worth what you pay for it. That’s the catch. A roll up often costs a net debit. A roll up-and-out adds more time, which can help offset the cost of moving to a higher strike, and may land near breakeven or with a small credit.

One example makes this plain. AAPL rose to $205 with the $200 strike call deep in the money. Rolling up-and-out to a June $210 strike lifted the cap from $204.10 to $214.00 for a $0.10 debit. That gives you more room if the stock keeps climbing, but it also means your capital stays tied up longer.

Rolling down: higher premium, lower rebound upside

If the stock has dropped and your focus shifts from upside to premium, rolling down pushes the trade more toward income. A lower strike usually brings in more premium and cuts your breakeven. The trade-off is simple: if the stock rebounds, your upside gets capped sooner, and assignment becomes more likely.

Before you roll down, check the new strike against your cost basis. If assignment happens below that level, you can lock in a loss. Rolling down can keep premium coming in, but it can also leave your capital stuck in a weak stock. Repeating the move too many times can backfire, since fees, slippage, and tied-up capital may eat away at the gain.

Each roll fixes one problem and creates another.

When Rolling Helps, When It Hurts, and How to Decide

Every roll solves one problem by creating another. That’s why the next step isn’t “should I roll?” by default. It’s deciding when to leave the trade alone.

Portfolio-level and behavioral mistakes to avoid

The most common rolling mistake is a mental one: refusing assignment after the stock has already reached a price you were fine accepting. That’s not a plan. It’s hesitation.

Anchoring to your original cost basis makes it worse. If you roll down below that cost basis, assignment can lock in a loss. At that point, the roll may not be fixing the trade. It may just be delaying the outcome.

Repeated rolls can also be a warning sign. Sometimes they point to a thesis that no longer holds up. And when you keep rolling, you keep capital tied up in the same position instead of putting it to work somewhere else.

Rolling is a tool for managing outcomes, not a guarantee of profit.

So the next move should come from a clear process, not a reflex.

A practical decision framework for self-directed investors

Start with one blunt question: would you open this exact position today at current prices? If the answer is no, the roll is a forced trade.

If the answer is yes, then check the numbers. A roll usually only makes sense when the new credit is at least 25% to 50% of the original premium collected. Below that, slippage and fees can eat up too much of the gain.

Timing matters too. Rolls tend to work better well before expiration, when there’s still enough extrinsic value to support a cleaner adjustment. It also helps to stay away from earnings or similar event risk unless you’re fully comfortable with a sharp move against the position.

| Decision Point | What to Ask |

|---|---|

| Stock thesis | Do I still want to own this stock at current prices? |

| Net credit | Is the new credit at least 25%–50% of the original? |

| Timing | Am I rolling well before expiration? |

| Event risk | Does this roll land over an earnings date? |

| Roll count | Have I already rolled this position once or twice? |

Using portfolio-aware analysis tools such as ThetaEdge

Portfolio context changes the call. Many investors look at each contract by itself and miss what the roll does to total income, position exposure, and capital flexibility.

ThetaEdge connects read-only to 80+ brokerages and shows covered call roll opportunities based on your actual holdings, with full risk, probability, and trade-off framing. It never executes trades or gives investment advice.

Conclusion: Rolling Is a Trade-Off, Not a Shortcut

Rolling a covered call changes your income, upside, and assignment risk. It does not change the stock's core risk. That's the key point. The decision should come from the trade-off in front of you now, not the setup you started with. Using portfolio intelligence can help clarify these trade-offs by providing real-time data on assignment probability and breakeven points.

Every roll adds friction. You take on more costs, stay in the position longer, and may run into earnings, dividend, and tax risk. A roll is not an escape hatch. It's just another decision with its own give-and-take.

Sometimes the best move is not to roll at all. If the shares can be called away at your target price, that may be the cleanest outcome. If the thesis breaks, or the risk-reward no longer looks better, close the position.

Covered call management works best when each choice is deliberate: roll, hold, accept assignment, or close based on what the current trade still supports.

FAQs

When should I roll instead of accept assignment?

Roll instead of accepting assignment when the underlying is at or just above your strike and you want to keep the position working a bit longer. The goal is usually one of three things: extend income, leave room for more upside, or reduce the chance of assignment.

In plain terms, rolling means the current covered call no longer matches what you want from the trade, but the broader setup still does. So rather than letting the shares get called away, you close the current option and open a new one.

This tends to make sense when the trade still lines up with your plan and the net credit looks good. Many traders look for that window when delta is between 0.55 and 0.65, or when they've already captured at least 50% of the premium.

How do I know if a roll is worth the extra time and cost?

A roll is usually worth a look if it gives you a meaningful net credit - often 25% to 50% of the original premium - and lands in the common 14 to 21 day window before expiration.

That part matters. A small credit can look fine on paper, then disappear once you factor in transaction costs and slippage.

You should also pay close attention to assignment risk. If the stock is near the strike, or if delta is above 0.70, the odds of assignment go up. In that setup, rolling can make more sense.

Can rolling a covered call lock in a loss?

No. Rolling a covered call does not, by itself, lock in a loss. What it can do is defer a loss or cut it, depending on market conditions and how you change the strike.