Stop Orders for Covered Calls: When and Why

Use stop-market and stop-limit orders with OTO coordination and the 20%/10% rule to manage covered-call risk and assignment.

Stop orders can help manage risk in covered call strategies, but they need to be thoughtfully applied to avoid complications. A covered call involves owning stock and selling a call option, generating income while capping upside potential. However, if the stock price drops or rallies sharply, managing both the stock and option legs is crucial to avoid excessive losses or unintended risks.

Here’s what you need to know:

- Stop orders trigger trades when a stock hits a specified price. They come in two types:

- Stop-market orders: Execute at the next available price once triggered.

- Stop-limit orders: Execute only at or better than your set price, but may not fill if the price moves too fast.

- Key risks include whipsaw effects (premature triggers during normal price swings) and execution uncertainty (orders may fill at worse-than-expected prices in volatile markets).

- Best practices:

- Use One Triggers Other (OTO) orders to manage both stock and call legs simultaneously, avoiding naked call risks.

- Set stops based on technical levels (e.g., below the 50-day moving average) or a fixed percentage (e.g., 7–8% drop from entry).

- For the call leg, use the 20%/10% rule: Buy back the call when its premium drops to 20% of the original value in the first half of the contract or 10% in the second half.

Stop orders can automate decisions, reduce emotional trading, and protect your portfolio. However, they require careful planning to avoid unintended outcomes. Tools like ThetaEdge can simplify tracking metrics like delta, breakeven, and assignment risk, helping you refine your approach while maintaining full control over your trades.

The Basics: Stop Orders and Covered Calls

What Is a Covered Call?

A covered call combines owning 100 shares of a stock with selling one call option against those shares. By doing this, you collect a premium upfront, but in return, you agree to sell your shares at the option's strike price if the buyer decides to exercise the contract.

This strategy tends to perform well in neutral-to-moderately-bullish markets - situations where you expect the stock to remain stable or rise slightly, but not skyrocket. The income you earn primarily comes from time decay (theta): as the option nears expiration, its value decreases, and you keep the premium. Grasping this structure is critical for understanding when stop orders might be necessary.

What Are Stop Orders?

A stop order is an instruction to your broker to execute a trade once a stock reaches a specific price. There are two main types you should know:

- Stop-market order: When the stop price is reached, the order becomes a market order and is executed at the next available price. While execution is guaranteed, the final price can vary, especially in volatile markets.

- Stop-limit order: When the stop price is hit, the order becomes a limit order. This means you set the minimum price you're willing to accept. However, if the stock's price moves past your limit too quickly, the order may not execute at all.

"Stop loss order: This is an order to sell a stock when its price declines to the stop price. At that point, the stop loss order becomes a market order (best available price)." - Dr. Alan Ellman, Founder, The Blue Collar Investor

Both types of stop orders play a key role in managing risk, especially when used alongside a covered call strategy.

Applying Stop Orders to a Covered Call Position

When managing a covered call, coordinating stops for both the stock and the option is crucial. Placing a stop only on the stock leg can leave you with an uncovered short call, which carries unlimited risk. To avoid this, you need to ensure both legs of the position are managed together.

A common solution is a One Triggers Other (OTO) order. This approach ensures that the first action - buying back the short call - happens before the second action - selling the stock. This keeps your position covered until the moment you exit.

For the call leg, setting a stop strategy involves using a Good 'Til Canceled (GTC) buy-to-close limit order. The goal is to close the call when its premium decays to 20% of its original value during the first half of the contract or 10% in the second half. This minimizes remaining risk at a low cost. By coordinating stops on both legs, you can effectively manage risk while maintaining control over your covered call strategy.

When to Use Stop Orders in Covered Call Strategies

Stop orders can be a useful tool in managing covered call strategies, but their effectiveness depends on market conditions and how they impact your positions.

Using Stops to Limit Losses on a Falling Stock

If a stock drops sharply, the premium you collected from the covered call provides only a small cushion. To protect against further losses, consider unwinding the position if the stock falls 7–8% below your entry price. Stops can be placed just below critical technical levels, like the 50-day moving average or a recent swing low, to avoid being prematurely triggered.

"The premium you collect provides a buffer, but it won't protect against a stock in freefall. There's no point in holding a $50 stock down to $35 just to collect another $1.50 in premium." - CashFlowMachine

Be cautious with stops that are set too tightly. A quick intraday dip followed by a recovery could trigger your stop unnecessarily, a phenomenon known as a "whipsaw", which can lead to avoidable losses.

Using Stops When the Stock Rallies Quickly

A rapid stock rally can increase the risk of assignment on your covered call. If the stock price moves above the call's strike price, your potential gains are capped, and the likelihood of assignment grows. To manage this, you can use a buy-to-close stop on the call. This allows you to repurchase the call before assignment and potentially roll the position forward, which is especially useful near ex-dividend dates.

Using Stops to Manage the Full Position at Once

Coordinating stops for both the stock and the call is essential to maintain the integrity of your covered call strategy. Selling the stock before closing the short call leaves you with a risky naked call position.

"The best stop order solution is to put in an OTO (one triggers other) order with the broker, specifying that if the stock reaches a certain price, the broker must close the trade by repurchasing the short calls and selling the underlying stock." - Financhill

Using an OTO order ensures that the call is closed first, followed by the sale of the stock. This approach keeps your covered call intact until the exit and simplifies decision-making during volatile market movements.

Benefits and Trade-Offs of Stop Orders in Covered Calls

When it comes to managing risk in covered call strategies, stop orders can play a pivotal role. However, as with any tool, they come with both advantages and drawbacks.

Key Benefits of Using Stop Orders

Stop orders are a practical way to manage risk automatically. If a stock begins to plummet, the premium collected from selling calls might not be enough to offset significant losses. A well-placed stop order can help you exit the position before a manageable loss spirals into something much worse.

Another advantage is the discipline stop orders enforce. By setting clear exit points ahead of time, you avoid the emotional temptation to "wait it out" or hope for a recovery. This approach can also free up capital faster. For instance, closing a position once you've captured 75% of the maximum premium allows you to reinvest sooner. Research even suggests this method can boost total income by as much as 42.5% compared to holding every position until expiration.

Trade-Offs to Keep in Mind

The most common issue with stop orders is the whipsaw effect. If you set your stop price too close to the current stock price, it might trigger during a routine dip, forcing you out of a position unnecessarily - only for the stock to recover shortly after.

There’s also execution uncertainty. When a stop order is triggered, it turns into a market order, which could fill at a price worse than you expected. Furthermore, stop orders don’t protect against overnight gaps. For example, if a stock opens significantly lower after bad earnings news, your order will execute at the opening price, which could be far below your stop level.

As Financhill explains:

"Stopping out of the position certainly is a better management tool than blindly holding onto a collapsing stock without action, in hopes of a recovery." - Financhill

Benefits vs. Trade-Offs at a Glance

| Benefit | Trade-Off |

|---|---|

| Automatic risk control: Limits losses before a stock drop overwhelms your premium cushion | Whipsaw risk: Normal price swings can trigger a stop on a stock that quickly recovers |

| Emotional discipline: Removes the urge to "hope" a bad trade turns around | Execution uncertainty: Stops become market orders and may fill at worse-than-expected prices |

| Capital efficiency: Closing at 75% profit lets you redeploy faster and increase annualized returns | Reduced income: Exiting early sacrifices the last 20–25% of potential premium |

| Naked call prevention: OTO orders close both legs, preventing exposure | Platform limitations: Some brokers may not support complex OTO or combination orders |

sbb-itb-a9ac3c2

How to Use Stop Orders Effectively with Covered Calls

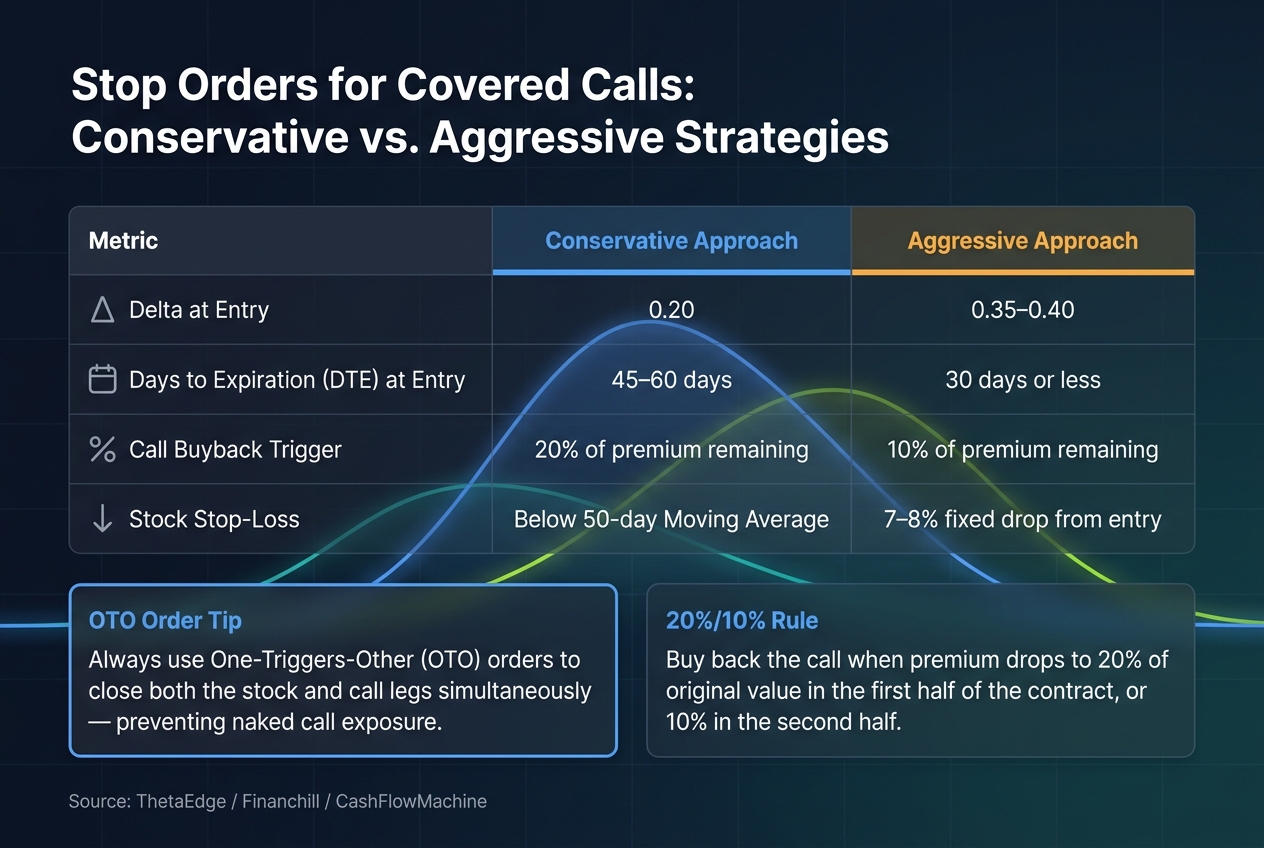

Stop Orders for Covered Calls: Conservative vs. Aggressive Approach

Managing stop orders effectively is crucial to maintaining the balance in a covered call strategy. It helps protect both the stock and the call option, ensuring you stay aligned with your risk management goals. Below are some practical approaches to refine stop placement for each leg of the position.

Setting Stops Based on Total Position Value

When calculating your breakeven, it’s important to factor in both the stock price adjustment and the cost of buying back the short call. As Financhill explains:

"The total debit, including the cost of buying back the short calls, is the real breakeven price."

For example, if the stock price drops by $1.00 and the call’s delta is 0.50, the option value may decrease by about $0.50. This relationship is key when determining your stop-loss level. Always include the cost of closing the short call when setting your stops to avoid miscalculating your net proceeds.

To prevent ending up with a naked short call, consider using an OTO (One Triggers Other) order, set as GTC (Good-Till-Canceled). This ensures that selling the stock automatically triggers the buyback of the short call.

Using Technical Levels to Place Stock Leg Stops

Technical support levels can serve as reliable benchmarks for setting stock stops. Placing your stop just below a key technical support level - such as the 50-day moving average, a swing low, or a well-respected trend line - can help avoid unnecessary triggers.

One touch of a support level doesn’t always warrant action. A decisive break of support, particularly when combined with negative news, is often a stronger signal to exit. As Financhill puts it:

"The breaking of support coupled with negative news seriously increases the threat level."

If you’re looking for a simpler method, setting a stop based on a 7–8% drop from your entry price is a popular approach. This method is easy to apply and helps keep losses manageable.

Setting Call Leg Stops Using Option Metrics

For the call leg, option-specific metrics provide clear guidelines for managing your positions. One effective rule is the 20%/10% rule: buy back the call when the premium drops to 20% of the original credit during the first half of the contract or 10% during the second half. At these levels, the remaining time value is minimal, and holding the position longer adds unnecessary risk.

Delta also plays a crucial role in deciding when to roll a covered call. Research from tastytrade highlights that the best time to roll is between 14–21 days to expiration (DTE), when the call’s delta reaches 0.60–0.70 - provided the roll results in a net credit. If the delta hits this range before expiration, it’s often a signal to act by either closing the position or rolling to a higher strike with a later expiration.

| Metric | Conservative Approach | Aggressive Approach |

|---|---|---|

| Delta at Entry | 0.20 | 0.35–0.40 |

| DTE at Entry | 45–60 days | 30 days or less |

| Call Buyback Trigger | 20% of premium remaining | 10% of premium remaining |

| Stock Stop-Loss | Below 50-day MA | 7–8% fixed drop |

How Portfolio-Aware Tools Like ThetaEdge Can Help

Understanding which metrics to monitor is important, but having those metrics directly tied to your actual positions takes things to another level. This is where a platform like ThetaEdge can streamline the process for covered call investors. By aligning risk metrics with your specific holdings, it brings a more precise approach to managing your stop placements.

Analysis Tailored to Your Portfolio

Most market scanning tools focus on opportunities across the broader market. ThetaEdge, however, zeroes in on covered call analysis for the stocks you already own. This personalized approach ensures that the insights and risk assessments are directly relevant to your portfolio, not just a generic watchlist.

For example, it provides clarity on metrics like your adjusted breakeven, assignment probability, and maximum potential outcomes. These details help fine-tune your stop placement decisions based on your actual cost basis.

Metrics to Refine Risk and Stop Decisions

ThetaEdge delivers key metrics - such as delta, theta, IV rank, probability of profit, and adjusted breakeven - that help you make smarter decisions. A 30-delta call (indicating about a 70% chance of expiring worthless) can guide how much room to leave for a trade, while a gamma spike in the final 7–10 days signals heightened assignment risk.

Full Control Over Your Trades

ThetaEdge connects securely to over 80 brokerages with read-only access, so it analyzes your holdings without executing trades. All stop orders must still be placed manually through your brokerage platform, ensuring you maintain complete control over every trade decision.

Conclusion: What to Remember About Stop Orders in Covered Calls

A well-thought-out stop order strategy is crucial for effectively managing covered calls. While stop orders help mitigate risk, they need to account for both legs of the position. Focusing solely on the stock leg could leave you exposed to the risks of a naked call.

To tackle this, consider using OTO (One-Triggers-Other) orders. These allow you to exit both the stock and call positions simultaneously if the stock drops below a key level. Instead of relying on arbitrary percentages, align your stops with meaningful technical indicators like the 50-day moving average. For example, many traders reassess their position if the stock falls 7–8% from the entry price.

On the call side, the 20%/10% rule is a practical guideline for taking profits. This means buying back the call when its premium shrinks to 20% of the original premium in the first half of the contract, or 10% in the latter half. Combining stops based on technical levels with the natural decay of option premiums helps protect against both steep losses and unexpected assignments.

"The traders who last are the ones who manage risk first and think about income second." - CashFlowMachine

To make these strategies easier to execute, tools like ThetaEdge can be invaluable. ThetaEdge provides insights into your adjusted breakeven, assignment probabilities, and key Greeks - all customized to your portfolio. These tools let you set informed stop orders with clarity, while still maintaining full control over your trades. Every decision remains yours, even as you leverage smarter tools to act with confidence.

FAQs

How do I avoid ending up with a naked call if my stock stop triggers?

To avoid the risks of holding a naked call, never sell your underlying stock while the short call remains open. If your stock's stop-loss order is activated, make sure to close both the stock position and the option position at the same time.

You can use tools like One-Cancels-Other (OCO) orders to manage this process. These orders ensure that when the stock is sold, the option is also bought to close, preventing unintended exposure to potentially large financial risks.

Should I use a stop-market or stop-limit order for covered calls?

When trading covered calls, the aim is to steer clear of ending up with a naked option position. This situation arises if you sell the stock without first closing out the short call option.

Using a stop-market order can help execute trades once a certain price is hit, but it might fill at less-than-ideal prices during sharp market declines. On the other hand, a stop-limit order guarantees a minimum price for execution but carries the risk of not being executed at all in fast-moving markets. To handle both sides of the trade more efficiently, many investors lean toward limit orders or automated strategies. These approaches provide a better balance between control and execution.

How do I set a stop that won’t get hit by normal price swings?

When setting stops, it’s important to leave room for normal price movements. Stops that are too tight can trigger unnecessarily, pulling you out of a position prematurely. A more flexible approach is to base your strategy on the stock’s behavior and your own risk tolerance.

For example, many investors use a 7%-8% decline in a stock’s price as a signal to reassess, rather than an automatic point of exit. Another option is to use contingent orders like One-Cancels-Other (OCO). This type of order allows you to link profit targets with risk management, offering a systematic way to navigate through market fluctuations without overreacting to short-term noise.