Capital Allocation vs. Position Sizing in Earnings Trades

Limit earnings exposure with portfolio-level allocation (10–15%) and trade-level risk (0.5–1%); diversify and reduce sizes in high volatility.

When trading options during earnings, managing risk comes down to two critical strategies: capital allocation and position sizing. Here's the difference:

- Capital Allocation: Decides how much of your total portfolio is exposed to earnings trades. For example, you might limit this to 10%-15% of your account.

- Position Sizing: Focuses on the risk per trade. Typically, you'd risk only 0.5%-1% of your account on a single trade to protect against large losses.

Together, these strategies ensure no single trade or series of trades can significantly harm your portfolio. By diversifying across sectors, staggering trade dates, and keeping risk levels low, you create a safer framework for navigating the unpredictability of earnings season.

Capital Allocation: Managing Portfolio-Level Risk

Capital allocation involves distributing your portfolio's capital across various strategies and sectors to manage overall risk. Think of it as setting boundaries to protect your portfolio from a single event - like a sector-wide selloff or a series of poor earnings reports - that could cause significant losses. This broader approach lays the groundwork for more detailed decisions, such as position sizing, which we’ll explore later.

It’s important to differentiate between capital and risk. In earnings trades, capital allocation refers to the buying power or collateral used across all positions. Risk, on the other hand, is the actual amount you could lose if multiple earnings trades go against you at the same time. By separating these concepts, you can ensure your portfolio is resilient enough to handle simultaneous losses without triggering forced liquidations.

"Diversification requires architecture, not just more tickers." – StrikeWatch EA Research Team

Many professional strategies suggest keeping only 30% to 50% of your total capital at risk at any time, with the rest held in cash or liquid reserves. For example, if your portfolio is worth $100,000, you’d aim to have no more than $30,000 to $50,000 exposed to potential losses across all open positions.

Setting Portfolio Limits for Earnings Trades

Earnings trades come with distinct risks, such as overnight price gaps and binary outcomes. To manage this, many traders allocate a specific portion of their portfolio - often 10% to 15% - exclusively to earnings strategies. This creates a buffer that shields the rest of the portfolio from the volatility earnings trades can bring.

Within this allocation, you should also impose position-specific limits. No single position should account for more than 5% to 10% of your total portfolio value. For instance, in a $100,000 portfolio with $15,000 allocated to earnings trades, each position should represent no more than $5,000 to $10,000 in notional value. Before entering new earnings trades, stress-test your portfolio against a potential 15%–20% market dip to ensure you can avoid margin calls. Additionally, keeping 20% to 30% of your portfolio in cash or Treasury bills provides the liquidity to navigate worst-case scenarios.

Diversification Across Sectors and Dates

Diversification is another critical layer of protection. It’s not enough to simply hold multiple tickers; you need to spread exposure across uncorrelated sectors. For example, holding earnings positions in NVIDIA, AMD, and Micron might seem diversified, but these stocks all belong to the semiconductor sector and are likely to move together if that sector faces challenges. True diversification involves allocating capital across sectors that are less likely to react in unison to the same economic events.

A common professional guideline is to limit sector exposure to 25% to 30% of your deployed capital. In a $100,000 portfolio with $50,000 deployed, you’d want no more than $12,500 to $15,000 concentrated in a single sector. If technology already accounts for 25% of your deployed capital, adding another tech earnings trade would increase your overall risk of correlation.

Timing also matters. As the StrikeWatch EA Research Team points out, "If three portfolio names report earnings in the same week, you have effectively concentrated the portfolio's binary-event risk regardless of how uncorrelated those stocks are the rest of the year." By staggering earnings dates, you reduce the likelihood of a single week’s results disproportionately affecting your portfolio. Always check that new positions don’t overlap with existing ones in terms of earnings dates.

Here’s an example to illustrate the importance of diversification: In a $100,000 portfolio, a 20% sector selloff might reduce your portfolio’s value by just 3.2% if your capital is spread across multiple sectors. However, if you’re heavily concentrated in one sector, the same selloff could result in a 9.6% loss - three times the impact. Over time, this difference can significantly influence your overall portfolio performance, highlighting why diversification is such a powerful tool for managing risk in earnings trades.

sbb-itb-a9ac3c2

Position Sizing: Managing Trade-Level Risk

Capital allocation sets the overall boundaries for your portfolio, but position sizing is where the rubber meets the road. It determines how much of your capital goes into each trade and, more importantly, how much you're prepared to lose if things don't go your way. This is where risk management becomes precise and personal.

Think of it this way: your broker might require $5,000 in buying power to hold a position, but the actual risk - what you'd lose if the trade hits its maximum loss - could be much smaller. The key is to size your trades based on potential loss, not just the capital requirement. This mindset helps ensure that no single trade jeopardizes your ability to keep trading, even in volatile markets.

"Position sizing is the single biggest determinant of long-term survival in options trading. It determines whether your strategy compounds wealth or blows up an account." – Matt, Options Trader, Flow Proof

Position Sizing for Earnings Trades

Earnings trades are a whole different ballgame. These events often bring large, unpredictable price gaps that can bypass traditional stop-loss orders. Because of this, professional traders typically lower their risk to 0.5% to 1% of total capital per trade, which is about half of what's used for more standard directional trades. For example, in a $100,000 account, you'd limit your risk to $500 to $1,000 on any single earnings trade.

How to Calculate Position Size

To keep things straightforward, here's a formula to calculate your trade size:

(Total Account Value × Risk % per Trade) ÷ (Max Loss per Contract or Share)

Let’s break it down with an example:

If you have a $100,000 account and are risking 1% on an earnings trade, your maximum acceptable loss is $1,000. Now, suppose you're trading an iron condor with a maximum loss of $400 per contract. You’d trade no more than 2 contracts ($1,000 ÷ $400 ≈ 2.5, rounded down).

For defined-risk spreads like vertical spreads or iron condors, this calculation works cleanly because you already know the maximum loss upfront. For instance, if you pay $2.50 for a debit spread, your max loss per contract is $250. If you sell a $5-wide credit spread for $1.50, your max loss is $350 per contract. And here's a golden rule: never size your trades based on the premium collected or the probability of profit. Even a trade with a 90% chance of success will eventually encounter that 10% loss scenario.

Adjusting for Volatility

Earnings trades often coincide with high implied volatility, which increases the risk of sharp, unexpected price swings (also known as gamma risk). During these periods, professional traders reduce their position sizes even further. For instance, if you'd normally risk 1% of your account on a trade, consider dropping to 0.5% when the VIX is elevated or when the implied volatility rank (IVR) of the stock exceeds 70%. This adjustment helps you absorb larger market moves without exceeding your risk tolerance.

Managing Losses and Concentration Risk

The 0.5% to 1% risk threshold is designed to protect you from significant drawdowns. Even if you face 10 consecutive losses, your account would only decline by 5% to 10%. Compare that to risking 20% per trade - three consecutive losses at that level could wipe out nearly half your account. By keeping losses small, you ensure your account remains intact for the long haul.

When trading during earnings season, avoid using hard stop-loss orders. Wide bid-ask spreads during volatile periods can trigger premature exits. Instead, consider mental stops based on the stock's price levels or rely on the defined risk of your spread. For example, if you're trading a debit spread and the stock breaches a key technical level, that could be your signal to exit, regardless of the option's quoted price.

Finally, even with properly sized trades, you need to watch for concentration risk. Holding multiple earnings trades in the same sector can expose you to correlated losses if the sector moves against you. To manage this, use beta-weighting to SPY equivalents. This approach helps you gauge whether your overall portfolio is too heavily tilted in one direction, preventing multiple trades from compounding your risk unnecessarily.

This method of precise scaling ties seamlessly into your broader portfolio risk management strategy.

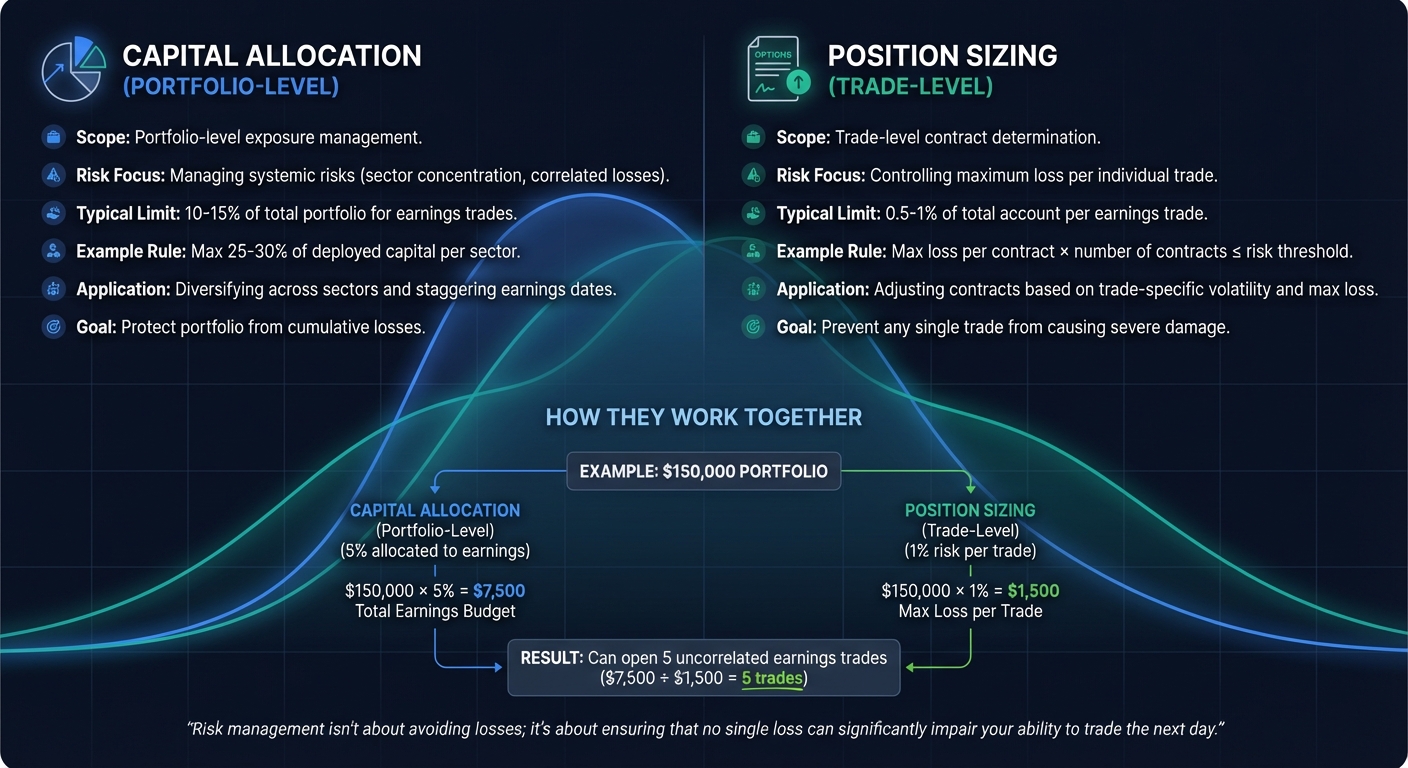

Comparing Capital Allocation and Position Sizing

Capital Allocation vs Position Sizing in Options Trading

When trading around earnings, managing both portfolio-wide exposure and individual trade risks is essential. Capital allocation determines how much of your portfolio is exposed overall, while position sizing focuses on limiting the risk tied to each specific trade.

Position sizing operates at the trade level. It involves calculating how many contracts to trade or calculating the risk per trade, based on its maximum possible loss. Capital allocation, on the other hand, sets the broader exposure limits for earnings trades. Together, they ensure that no single trade or series of trades can cause significant harm to your account.

"Risk management isn't about avoiding losses; it's about ensuring that no single loss can significantly impair your ability to trade the next day." – ImpliedOptions Research

The two approaches address different aspects of risk. Capital allocation protects the portfolio from cumulative losses, considering factors like sector concentration and correlated risks. Position sizing, meanwhile, focuses on preventing one bad trade - whether from a sharp drop in implied volatility or an unexpected gap down - from causing outsized damage. The table below highlights the key differences between these strategies.

Comparison Table

| Aspect | Capital Allocation | Position Sizing |

|---|---|---|

| Scope | Portfolio-level exposure management | Trade-level contract determination |

| Risk Focus | Managing systemic risks | Controlling maximum loss per trade |

| Application | Diversifying across sectors and dates | Adjusting for trade-specific volatility |

Combining Capital Allocation and Position Sizing for Earnings Trades

Integrating capital allocation and position sizing into your strategy creates a layered approach to managing risk. These two elements work together: capital allocation sets a limit on how much of your portfolio is exposed to earnings trades, while position sizing ensures that no single trade can cause severe losses, even in the worst-case scenario.

This combination is especially important for earnings trades, where price movements can be highly unpredictable and extreme. Both controls act as safeguards, helping to manage the volatility and potential risks that come with these trades.

Example: Combining Allocation and Sizing

Let’s say you have a $150,000 portfolio. You might allocate 5% of it - $7,500 - for earnings trades. This becomes your "earnings budget", the maximum amount you’re willing to commit across all active positions.

Within that $7,500, you could apply a 1% rule for individual trades, meaning no trade should risk more than $1,500. For example, if you’re considering selling a cash-secured put with a $200 strike price, the potential maximum loss could be $20,000 - the full notional value. This far exceeds your $1,500 risk threshold. To address this, you could opt for a defined-risk strategy, like a put spread, which caps the potential loss and keeps it within your $1,500 limit.

Using this framework, you could open five unrelated earnings trades, each with a $1,500 risk cap (5 × $1,500 = $7,500 total risk). This ensures you stay within both your overall allocation and per-trade risk limits. Once this structure is in place, you can focus on refining your parameters as market conditions change.

Adapting to Market Conditions

After setting your allocation and position sizing, keep an eye on market shifts and adjust your strategy as needed. For example, during periods of higher implied volatility or a rising VIX, consider reducing your position sizes. Increased gamma risk during these times can lead to faster and larger losses.

Pay close attention to your portfolio Greeks, particularly vega. If you hold five earnings positions and your total portfolio vega is –$800, a 10-point spike in implied volatility could increase your overall risk by $8,000. This type of concentration risk might not be obvious when evaluating trades individually. To avoid this, use beta-weighting to convert all your positions into "SPY equivalents." This helps ensure you’re not unintentionally making a large directional bet on the market through multiple positions.

Finally, maintain a healthy cash reserve - around 50% to 70% of your portfolio. Many experienced traders keep the majority of their accounts in cash, using only 30% to 50% for active trades. This liquidity provides flexibility for handling assignments, making adjustments, or seizing new opportunities without being forced to close positions under unfavorable conditions during market stress.

Conclusion

Capital allocation and position sizing are two key tools that work hand-in-hand to protect your portfolio during earnings trades. While capital allocation limits your overall exposure - typically keeping it around 10% to 15% of your account for earnings events - position sizing ensures that individual trades carry minimal risk. Together, they act as safeguards, limiting both total exposure and the impact of any single trade.

This combined strategy helps avoid concentration risk, especially during periods of market stress. For instance, multiple trades in the same sector or earnings week could behave like a single oversized bet, amplifying potential losses. As ImpliedOptions Research explains, "Risk management isn't about avoiding losses; it's about ensuring that no single loss can significantly impair your ability to trade the next day".

In earnings trades, these controls establish discipline even in highly volatile conditions. Spikes in implied volatility and tail risks can challenge even high-probability setups, but a structured approach allows probabilities to play out over the long run rather than letting short-term setbacks disrupt your strategy.

Recognizing the difficulty of managing these factors manually, platforms like ThetaEdge simplify the process. By monitoring your holdings, calculating portfolio Greeks, and providing a clear analysis of risks and trade-offs, ThetaEdge offers AI-powered insights to help you evaluate each opportunity before committing capital. This turns abstract risk-management principles into practical, portfolio-specific decisions, enabling you to make more confident and informed choices. Together, these practices help protect your portfolio while supporting smarter, more disciplined trading.

FAQs

What’s the simplest way to set an “earnings budget” for my account?

To establish an "earnings budget", designate a small, fixed percentage of your total account capital - usually between 1% and 5% - for earnings trades. For instance, if you have a $50,000 account and decide to risk 2%, your budget for these trades would be capped at $1,000. This percentage-based strategy helps you manage risk effectively, aligns with your comfort level, and avoids overexposing your portfolio. Sticking to this disciplined approach ensures your trading remains within safe, predetermined boundaries.

How do I size an options trade using max loss (not premium or buying power)?

To determine the size of an options trade using maximum loss, start by deciding how much of your portfolio you're willing to risk on a single trade - commonly between 1% and 5%. Once you have this risk limit, divide it by the maximum loss per contract to calculate how many contracts you should trade.

For instance, if your portfolio is worth $100,000 and your risk tolerance is 2% ($2,000), adjust your position size so that your total potential loss doesn't exceed this $2,000 threshold.

How can I avoid hidden correlation when I have multiple earnings trades open?

Managing portfolio-level risk is critical when dealing with multiple earnings trades. Focusing solely on individual positions can leave you exposed to hidden correlations, especially during periods of market volatility. Pay close attention to key Greeks like delta, theta, and vega, as these metrics can help pinpoint areas where your portfolio might be overly concentrated or vulnerable.

Correlations between trades can intensify quickly in turbulent markets, so it's important to account for how your positions interact. Having predefined adjustment triggers and sticking to a written risk management plan can help you navigate these complexities. By doing so, you can address systemic risks effectively and ensure your trades are managed with a broader, more informed perspective.