Volatility Spikes: Impact on Covered Call Premiums

Explains how volatility spikes inflate covered call premiums, raise assignment risk, and recommends strike, expiration, and rolling strategies to manage income and loss.

When market volatility rises, covered call premiums increase significantly. This happens because implied volatility (IV) - the market's forecast of potential price swings - directly influences option pricing. Higher IV means higher premiums, offering income opportunities for option sellers. However, it also raises risks, including a greater chance of assignment and potential losses on the underlying stock.

Key takeaways:

- Volatility spikes: Triggered by events like economic reports or geopolitical tensions, these cause rapid IV increases.

- Higher premiums: Elevated IV boosts the extrinsic value of options, leading to richer premiums.

- Risks involved: Increased assignment likelihood and potential stock price declines.

- Strategies to manage risks: Adjust strike prices, use shorter expirations, and consider rolling calls to balance income and risk.

Understanding these dynamics helps you navigate volatile markets while maximizing income potential from covered call strategies.

How Volatility Spikes Change Covered Call Premiums

When volatility spikes, covered call premiums often see a sharp increase. This happens because the extrinsic value of the option - reflecting time and uncertainty - grows significantly. While the intrinsic value (the amount by which a call is in-the-money) stays the same, the market's anticipation of larger price swings inflates the extrinsic portion. This effect is driven by Vega, which measures how much an option's premium changes for every 1% shift in implied volatility (IV). As a result, elevated premiums are a natural byproduct of heightened market uncertainty.

Higher Premiums During Volatility Spikes

During periods of high volatility, premiums can rise dramatically. For example, when Nvidia (NVDA) trades at $140, a one-month $150 strike call might see its premium jump from $2 in a calm market to $5 or more during a volatile event like earnings week.

A useful rule of thumb is that if a one-month at-the-money option offers a return exceeding 6–7%, the market is pricing in a significant price move before expiration. This "volatility risk premium" rewards option sellers because implied volatility typically exceeds realized volatility by about 3–4 percentage points, compensating for the added uncertainty.

Greater Assignment Risk

The downside of higher premiums is a greater chance of assignment. When volatility spikes, the probability of your stock hitting or exceeding the strike price increases. The same uncertainty that inflates premiums also fuels sharp price movements, making it more likely that options move in-the-money. This could lead to your shares being called away, especially during a strong rally past your strike price. To mitigate this, choose strike prices that align with your acceptable selling levels - prices where you'd be comfortable parting with your shares even if they continue to climb. Balancing the appeal of higher premiums with the risk of assignment is key to managing this trade-off.

Risk of Unrealized Losses

While higher premiums provide a buffer, they don't fully protect against steep declines in stock prices. For instance, on December 18, 2024, when the VIX surged 74% to 27.62, many stocks saw significant drops despite the rise in premiums. As a result, the income from premiums may not be enough to offset losses on the underlying stock. As Investopedia explains:

"If the stock's price falls sharply, the premium collected may not be enough to offset the loss on the underlying stock, resulting in an unfavorable outcome."

This highlights the importance of monitoring both Theta (time decay) and Vega (volatility risk). A common approach is to target options with an implied volatility of 50% or more and a Theta-to-Vega ratio above 0.25. This balance helps optimize the trade-off between risk and reward.

sbb-itb-a9ac3c2

Strategies for Managing Covered Calls During Volatility Spikes

When markets become volatile, managing covered calls requires thoughtful adjustments. While higher volatility inflates premiums, it also increases assignment risk and amplifies price fluctuations. Here are three approaches to help balance income generation with risk management during these turbulent times.

Adjust Strike Prices and Expirations

Volatility opens the door to setting strike prices further out-of-the-money (OTM) while still locking in attractive premiums. This reduces assignment risk, as higher implied volatility (IV) means you can collect sizable premiums even with safer, less aggressive strikes. For instance, a call with a 0.25 delta typically has about a 25% chance of being assigned, making it a common choice during uncertain markets.

Shorter expirations can also work to your advantage. In high-IV conditions, a two-week option may yield premiums comparable to what a 30-day option would offer in calmer markets. This lets you cycle through positions more frequently, potentially reinvesting for higher returns. Many experienced traders aim for expirations 30–45 days out with strike deltas between 0.15 and 0.35, striking a balance between income potential and risk management.

Use Rolling Strategies

If adjusting strikes alone isn’t enough, rolling your covered calls can provide additional flexibility. Rolling involves closing your current call and opening a new one with different terms, allowing you to adapt to shifting market dynamics.

A common rolling strategy is to act after capturing 50% of the maximum profit or when there are 21 days left to expiration - when gamma risk, or the sensitivity to price changes, increases significantly.

During rallies, rolling up to a higher strike with a later expiration can capture elevated premiums while leaving room for further stock appreciation. On the flip side, if the stock price drops, rolling down and out (to a lower strike and later expiration) can help offset losses by bringing in additional premium.

Use Professional Analysis Tools

In volatile markets, technology can provide a critical edge. Platforms like ThetaEdge offer real-time tracking of key metrics such as Delta, Theta, and Vega, helping you make informed adjustments when needed. For instance, monitoring Implied Volatility Rank (IVR) can reveal when options are unusually expensive compared to historical norms - typically when IVR exceeds 35.

ThetaEdge also calculates the Theta-to-Vega ratio, which can guide you toward options with a better balance of income and risk. A ratio above 0.25 is often considered favorable. During a recent volatility spike, when the VIX surged 74% in a single day, professional tools highlighted that short-term options saw extreme premium expansion, while longer-dated options remained relatively stable. Features like the Thetix AI assistant further streamline decision-making by offering tailored portfolio insights and actionable recommendations.

Covered Call Premiums in Different Market Conditions

Covered Call Premium Comparison: Low vs High Volatility Markets

Market conditions play a big role in determining covered call premiums. In calmer markets, premiums tend to be lower, while volatile markets can significantly boost them. Understanding how implied volatility (IV) influences premiums is key to deciding when to write calls and what kind of returns you might expect. As noted earlier, volatility spikes not only increase premiums but also heighten the risk of assignment. Let’s take a closer look at how these dynamics unfold in different scenarios.

Premium Comparison: Low IV vs. High IV

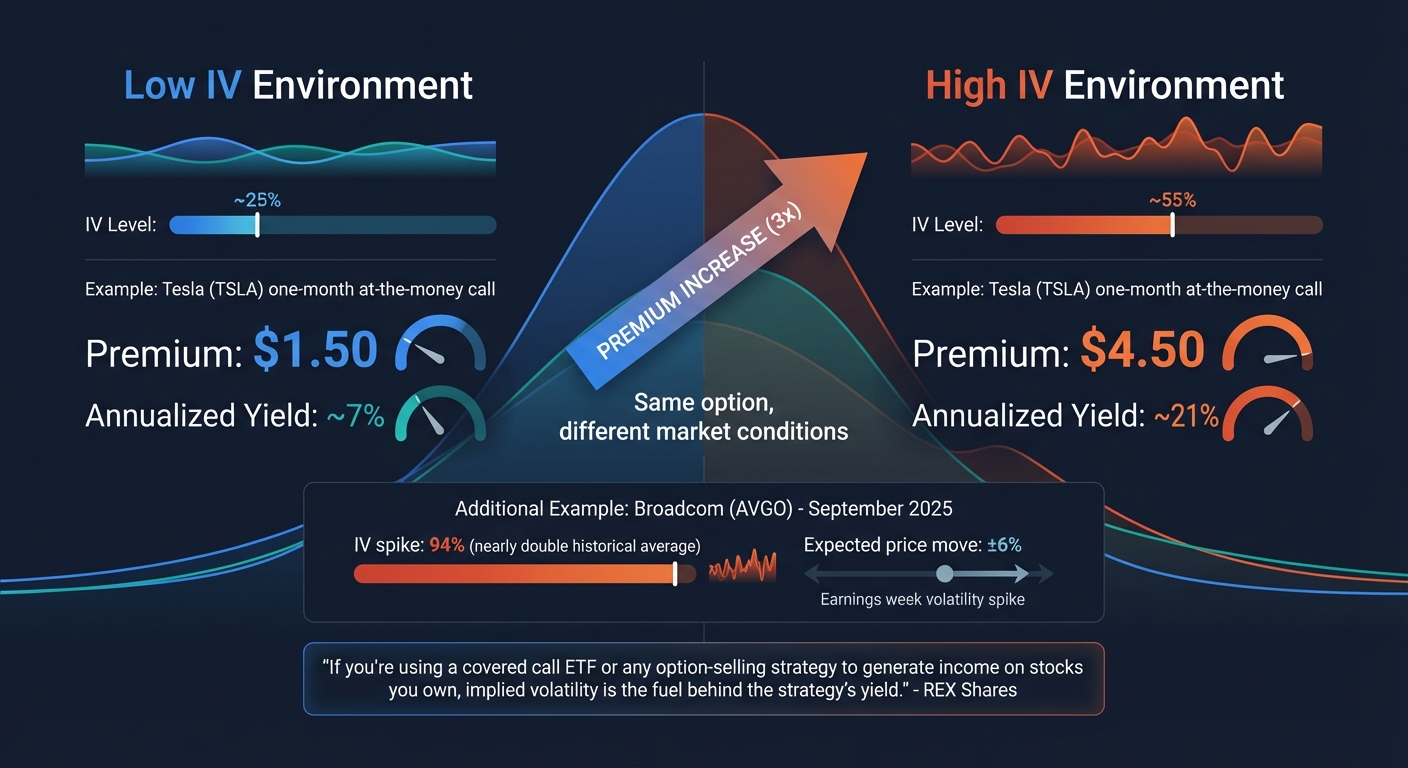

When markets are steady, premiums are modest. During uncertain or volatile times, they can skyrocket. Take Tesla (TSLA) as an example. In a calm market with IV around 25%, a one-month at-the-money call generated a $1.50 premium, translating to about a 7% annualized yield. However, in a more volatile market with IV spiking to 55%, the same call brought in a $4.50 premium, offering a much higher annualized yield of approximately 21%.

"If you're using a covered call ETF or any option-selling strategy to generate income on stocks you own, implied volatility is the fuel behind the strategy's yield." – REX Shares

Low IV generally indicates expected stability, while high IV reflects anticipated turbulence, which inflates the time value of options.

This trend isn’t limited to Tesla. In September 2025, Broadcom (AVGO) saw its implied volatility soar to nearly 94% just ahead of an earnings report - almost double its historical average. This spike reflected expectations of a potential ±6% price move. Option sellers enjoyed hefty premiums during this period but also faced significantly higher assignment risks.

High IV conditions can dramatically boost your income potential, sometimes doubling or tripling it. However, this comes with increased market stress and uncertainty. On the other hand, low IV periods offer smaller premiums but with reduced risk. Keeping an eye on IV percentile rankings can help you gauge whether current premiums are elevated compared to a stock’s historical norms.

Conclusion

Volatility spikes can significantly impact covered call strategies, offering both opportunities and challenges. They boost premium income but also increase the risk of assignment. Navigating these shifts effectively means balancing the potential for richer premiums with strategies to manage assignment risks.

Key Strategies to Consider

When volatility surges, adjusting your approach is crucial. Set strike prices further out-of-the-money to take advantage of higher premiums while reducing the likelihood of assignment. Employ rolling strategies to adapt: roll up to capture more upside, roll out to extend the contract's duration, or roll down for added downside protection as market conditions demand. Experienced traders often aim for a Theta-to-Vega ratio above 0.25 and focus on achieving 2–4% monthly returns during volatile periods, avoiding the temptation to chase higher returns of 6–7%.

"Professional traders consistently prioritize survival over performance, understanding that steady risk management leads to long-term success." – TradeStation

Tools like ThetaEdge can simplify this process by providing detailed analysis of your portfolio’s Greeks, assignment probabilities, and data-driven recommendations for strike prices and rolling opportunities tailored to current market conditions.

Stay Disciplined and Informed

Beyond strategy tweaks, staying vigilant about market signals is key. Volatility tends to revert to its mean - historical trends show that 90% of VIX spikes above 30 subside within three months. This makes timing critical, as elevated premiums won’t last indefinitely. Regularly monitor implied volatility rank (IVR), aiming to sell when IVR is at or above 35, and keep your position sizes conservative - just 1–2% of your total capital per trade during turbulent periods. Establish clear exit rules, such as closing trades when they reach 50–75% of their maximum profit, and roll positions when the short call's delta climbs above 35–40.

With a disciplined approach and the right tools, volatility spikes can transition from being a source of stress to an opportunity for consistent income generation.

FAQs

How can I tell if a covered call premium is “too high” because IV is inflated?

When evaluating whether a covered call premium is elevated due to high implied volatility (IV), it’s helpful to compare the current IV to the stock’s historical volatility (HV). If the IV is significantly higher than the HV, it often indicates that the premium is factoring in market uncertainty or potential upcoming events.

You can also look at broader measures like the VIX or similar volatility indices. These tools provide insight into whether the increased premium aligns with overall market conditions or if it exaggerates the stock’s actual risk.

What’s the best way to avoid getting assigned during a volatility spike?

When dealing with a sudden spike in volatility, it’s important to take steps to reduce the risk of assignment. One approach is to avoid selling covered calls during periods of high implied volatility. While the premiums may be tempting, they come with a higher chance of your shares being called away.

If the stock price starts creeping toward your strike, consider adjusting or closing your position early to avoid unwanted outcomes. Another option is to select strike prices further out-of-the-money, giving yourself more breathing room. You could also roll your calls to later expiration dates or higher strike prices to create additional space for potential price swings. These strategies help you manage risk while staying in control of your portfolio.

How do I choose strikes using delta and the Theta-to-Vega ratio?

When selecting strike prices, delta plays a key role in balancing the premium you earn with the risk of assignment. For covered calls, a delta in the range of 0.3 to 0.5 is often a popular choice, as it offers a reasonable trade-off between income and the likelihood of your shares being called away.

Next, consider the Theta-to-Vega ratio. A higher ratio indicates that time decay (Theta) has a stronger influence compared to changes in volatility (Vega), which can be beneficial if you're looking to capitalize on time decay. On the other hand, a lower ratio means the position is more sensitive to volatility shifts, which could lead to larger swings in value during volatile markets.

By combining these two metrics - delta and the Theta-to-Vega ratio - you can fine-tune your strategy to optimize premium collection while keeping risk in check, especially during periods of market turbulence.